Researcher Identifies Five Major Retirement Risks

What is the most serious risk to our retirement?

Retiring can be exciting, but it’s important to recognize the risks and plan accordingly. Recent research has identified five major retirement risks that retirees must address—from investments to healthcare needs. These issues are not equally concerning, so understanding the most severe ones can help you adjust your retirement strategy. In this blog post, we’ll look at these five risks in detail, assess their potential impact on retirement planning decisions, and offer advice on how best to manage them. Read on for a comprehensive review of the most significant retirement risk areas!

These risks encompass a diverse array of financial risks and challenges:

- Longevity: Outliving Your Money

- The US National Debt

- Social Security

- Medicare & Unplanned Healthcare Expenses

- Inflation & Market Volatility

Retirement Risk #1: Longevity

Outliving Your Money

Americans are spending more years in retirement, making longevity an increasingly important financial consideration. In 1940, a 65-year-old man could expect to live approximately 11.9 more years, while a 65-year-old woman could expect another 13.4 years. According to the latest life tables used in the 2026 Social Security Trustees Report, a 65-year-old man can now expect to live approximately 18.1 additional years, while a woman of the same age can expect another 20.7 years. The nation’s older population is also expanding rapidly. The number of Americans age 65 and older reached approximately 61.2 million in 2024 and is projected to reach roughly 77 million by 2034 (1)

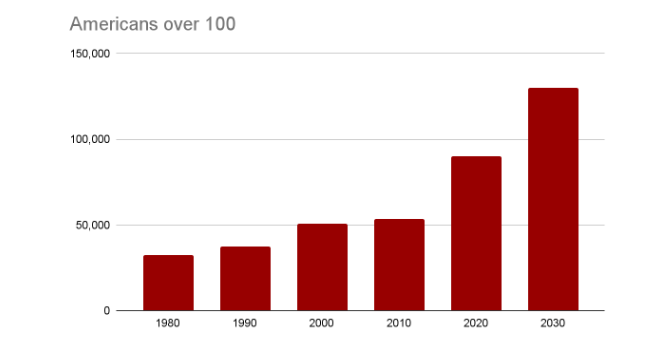

There are over 90K centurions – up from ~53k in 2010.

Living Longer Than You Planned

According to the U.S. Census Bureau, the number of Americans age 100 and older increased by approximately 50%, from 53,364 in 2010 to 80,139 in 2020. The Census Bureau’s latest national population projections estimate that the centenarian population will reach approximately 110,800 in 2026 and 134,000 by 2030.

The oldest members of the baby boom generation, born in 1946, will begin turning 100 in 2046. As more surviving baby boomers reach advanced ages, the centenarian population is projected to grow substantially, reaching approximately 519,000 by 2060.

According to the U.S. Census Bureau, the number of Americans age 100 and older increased by approximately 50%, from 53,364 in 2010 to 80,139 in 2020. The Census Bureau’s latest national population projections estimate that the centenarian population will reach approximately 110,800 in 2026 and 134,000 by 2030.

The oldest members of the baby boom generation, born in 1946, will begin turning 100 in 2046. As more surviving baby boomers reach advanced ages, the centenarian population is projected to grow substantially, reaching approximately 519,000 by 2060 (2)

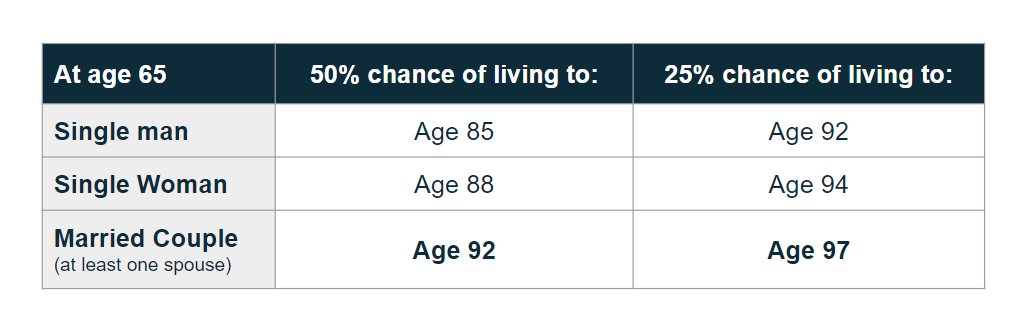

Will you live to be 90+?

Upon reaching 65, individuals face varying life expectancy probabilities. For a single man, there’s a 50% chance of living to age 85 and a 25% chance of reaching 92. On the other hand, a single woman has a 50% chance of living to 88 and a 25% chance of getting to 94.

The dynamics of longevity risk shift slightly for a married couple in which at least one spouse is present. The chances of one spouse reaching 92 are 50%, and the probability of reaching 97 is 25% (3). These figures highlight the diverse range of potential lifespans individuals and couples might encounter as they navigate retirement.

How to Prepare Your Money to Outlive Your Life Expectancy

What strategies can you employ to counter the extra costs of an extended lifespan?

- Consider trimming your budget and reducing living expenses

- Adjust your investment strategy and plans accordingly

- Extend your working years beyond your initial plan

Retirement Risk #2: The US National Debt

The US National Debt, encompassing the cumulative impact of budget deficits, has surged significantly over the past 15 years, tripling in magnitude. Presently standing at an astonishing figure of over 39+ trillion dollars, this mounting debt highlights a concerning trend. The absence of a budget surplus since 2001 has contributed to this escalating financial burden, underlining the challenge of reining in the nation’s financial obligations. Addressing this issue becomes increasingly vital to ensure the country’s long-term economic stability and sustainability.

How much is the federal budget?

- Defense Budget Expenses: This refers to the portion of the federal budget allocated to military operations, personnel, equipment, research, and other national defense activities. The Department of Defense’s fiscal year 2026 budget request totals approximately $961 billion, including $113 billion provided through the 2025 Reconciliation Act.

- Social Security Program and Disability Pensions: Geared towards offering financial stability to retirees and individuals with disabilities, the cumulative outlay for Social Security and related expenses amounts to approximately $1.2 trillion.

- Medicare/Medicaid and Other Healthcare Programs: Collectively, healthcare benefit programs, encompassing Medicare and Medicaid, receive a designated budget of $1.4 trillion.

- Other Miscellaneous Expenses: These encompass a range of categories, including transportation infrastructure development, comprehensive veterans’ benefits and support, international affairs engagements, and the funding of public education initiatives.

For fiscal year 2026, the federal government is projected to spend approximately $7.4 trillion and collect approximately $5.6 trillion in revenue, resulting in a projected budget deficit of about $1.9 trillion. (4)

National Debt Potential Solutions

To address the existing national debt, a viable approach involves generating a surplus, achievable through either of the following avenues:

- Increasing revenue by adjusting taxation

- Implementing prudent budget reductions across various expenditure categories

Retirement Risk #3: Social Security

The Social Security Board of Trustees’ 2026 annual report projects that the combined reserves of the Old-Age and Survivors Insurance and Disability Insurance trust funds will be depleted in 2034 if Congress does not act. At that point, ongoing program income would be sufficient to pay approximately 83% of scheduled benefits. The retirement-focused Old-Age and Survivors Insurance Trust Fund alone is projected to be depleted sooner, in the fourth quarter of 2032, when approximately 78% of scheduled benefits would remain payable. (13)

Will Baby Boomers Bankrupt Social Security?

The baby boomer generation, a significant demographic that emerged during the 1960s and 1970s, was born between 1946 and 1964. This expansive group started turning 62 in 2008. As we look ahead to 2031, the youngest boomers will have surpassed the full retirement age for Social Security, set at 67 for those born in 1960 or later. This milestone will coincide with a population of 75 million individuals aged 65 and above—almost double the 39 million seniors in 2008. (4)

Social Security Funds

At the end of 2025, the Social Security trust funds held approximately $2.56 trillion in combined reserves, down from about $2.72 trillion one year earlier. Of that amount, approximately $2.34 trillion was held in the Federal Old-Age and Survivors Insurance Trust Fund, which supports retired workers, survivors, and their families, while approximately $223 billion was held in the Federal Disability Insurance Trust Fund, which supports eligible workers with disabilities and their families.

Together, these two funds are commonly referred to as the OASDI trust funds. Their reserves are invested in interest-bearing U.S. Treasury securities and are used when current program income is insufficient to cover scheduled benefits and administrative expenses. (5)

How Social Security Works

Three distinct sources of income support Social Security’s financial foundation. These include payroll taxes, interest generated from surplus funds held by the Treasury, and taxes levied on benefits received by current beneficiaries.

The primary funding source for the Social Security trust funds is payroll taxes. In 2026, employees and employers each contribute 6.2% of covered earnings, up to the taxable maximum of $184,500, while self-employed workers pay the combined 12.4% rate. According to the latest available annual data, net payroll tax contributions accounted for approximately 91.3% of total trust fund income in 2025. The remaining income came primarily from interest earned on trust fund securities and federal income taxes imposed on certain Social Security benefits. (6)

In 1945, there were 41.9 workers per Social Security beneficiary.

Social Security Trust Fund

At present, approximately 2.8 workers are supporting each beneficiary. However, by 2032, this ratio will decline to about 2.3 workers per beneficiary. Meanwhile, life expectancy has increased, leading to longer benefit durations.

As the baby boomer generation enters retirement, the number of benefit recipients will rise significantly, while the taxpaying population will represent a smaller share of society. The Social Security Trust Fund is anticipated to cover scheduled benefits until around 2034. Beyond that, the fund is projected to provide only 78% of the planned benefits with ongoing tax revenues. (7)

Depletion of Social Security

The evolving demographics pose a challenge, as the system may face a funding shortage if inflows are insufficient relative to outflows. As long as employees pay taxes, funds will be available to disburse benefits.

Yet, the imbalance arising from a smaller workforce contributing and a larger beneficiary pool receiving benefits might result in reduced payouts unless Congress takes proactive measures to restore the fund’s resources before that point.

Potential Social Security Solutions

Raise the full retirement age for Social Security benefits: In the upcoming years, the full retirement age is set to increase to 67 for individuals born in 1960 and beyond. Discussions suggest it could be raised to 69, or even 70, given the considerable increase in lifespans since Social Security’s inception.

Raise the payroll tax rate to 15.08%: This proposal would increase the combined tax rate of 12.4% by 2.68%. Both employers and employees would contribute 7.54% each, up from the current 6.2%.

Raise or eliminate the payroll tax cap: In 2026, Social Security payroll taxes apply to earnings up to $184,500, an increase from $176,100 in 2025. This taxable maximum generally rises each year based on growth in the national average wage. Raising or eliminating the cap would subject more high-income earnings to Social Security taxes and could significantly reduce the program’s long-term funding shortfall, although the financial effect would depend on whether those additional taxed earnings also generate higher future benefits.

Our aim is not to provide a definitive solution to the Social Security depletion issue but to present potential strategies to navigate its potential challenges. The resolution to the long-term funding concern for Social Security might entail a combination of approaches, such as raising Social Security taxes, adjusting benefit levels, and aligning the retirement age with rising life expectancy. (8)

Find out more about Social Security here.

Retirement Risk #4: Medicare & Unplanned Healthcare Expenses

Viewing the payment of anticipated and unforeseen healthcare and medical costs as a fundamental necessity is crucial. Here are vital factors:

- Understanding the coverage and expenses linked to Medicare Parts A, B, C, and D

- Taking into account out-of-pocket healthcare charges not encompassed by Medicare, like premiums, deductibles, copays, as well as hearing, dental, and vision expenditures

- Evaluating the possibility of requiring long-term care

It’s projected that Medicare will cover only approximately 60% of retirement medical expenses. According to the Center for Retirement Research, couples aged 65 and above typically incur an average annual expenditure of around $7,600 on Medicare premiums and copays. (9)

Medicare Coverage

Medicare offers a comprehensive framework for healthcare coverage during retirement, with various parts addressing specific needs. Medicare Part A covers basic hospital care, while Part B covers outpatient care, including doctor visits and diagnostic tests.

Medicare Part C, also known as Medicare Advantage, is a private alternative that combines Part A and Part B coverage and provides additional benefits. Part D, on the other hand, focuses on prescription drug coverage.

For those seeking additional support, Medicare supplement plans, or Medigap, offer private insurance that helps mitigate out-of-pocket expenses such as copays, coinsurance, and deductibles. This diversified approach allows retirees to tailor their healthcare coverage to their needs.

Despite its extensive coverage, Medicare does not cover certain aspects of healthcare. Dental care, eye exams, hearing aids, acupuncture, and cosmetic surgeries are not covered by original Medicare. Long-term care is not part of Medicare’s coverage. If you anticipate the need for long-term care for yourself or a family member, it is advisable to explore a separate long-term care insurance policy to ensure comprehensive coverage of health care expenses.

Medicare Part A

Medicare Part A covers short stays at a Skilled Nursing Facility (SNF). Here is the breakdown of covered costs depending on the length of stay:

- Days 1 through 20: Part A pays the entire cost of any covered services

- Days 21 through 100: Part A pays for all covered services, but you’re now responsible for a daily coinsurance payment

- After 100 days, Part A pays nothing. You’re accountable for the entire cost of SNF services.

Medicare Part A provides comprehensive coverage for most hospice care expenses, though minor copays may apply to respite care, medical bills, or prescriptions. Remember that Medicare does not cover room and board costs during hospice care. Custodial care, which involves aid with daily activities such as eating, dressing, and personal hygiene, is not covered either. This type of care is a significant aspect of services offered in nursing homes and assisted living facilities. (10)

Long-Term Care

Statistically, current 65-year-olds face a substantial 70% likelihood of requiring long-term care assistance at some juncture. Among this group, about 69% may need such services for three years, while a notable 20% could require assistance for five years or more.

It’s important to note that typical health insurance plans do not encompass long-term care provisions. This applies to both employer-provided health coverage and federal healthcare programs like Medicare. While Original Medicare doesn’t include long-term care coverage, it may cover up to 100 days of skilled nursing care or rehabilitation in a nursing facility. Beyond this timeframe, beneficiaries are responsible for the entire cost of long-term care services. (11)

Long-Term Care Insurance

Without long-term care insurance or another dedicated funding strategy, the cost of care can place a significant strain on retirement savings. According to the latest national survey data available in 2026, median annual long-term care costs range from approximately $24,700 for adult day health care to nearly $129,600 for a private room in a nursing home.

The national median costs reported for 2025 are:

- Nursing home, semi-private room: $315 per day, or approximately $9,581 per month, and $114,975 per year

- Nursing home, private room: $355 per day, or approximately $10,798 per month, and $129,575 per year

- One-bedroom assisted living unit: approximately $6,200 per month, or $74,400 per year

- Non-medical in-home caregiver: approximately $35 per hour, or $80,080 per year, based on 44 hours of care per week

- Adult day health care: approximately $95 per day, or $24,700 per year, based on five days of care per week (12)

Actual costs can vary significantly depending on location, the amount of care required, and the services provided. Long-term care insurance may help cover some of these expenses, depending on the policy’s benefits, exclusions, waiting period and coverage limits.

Retirement Risk #5: Inflation & Market Volatility

Inflation is the gradual increase in the cost of goods and services over time. Various factors, such as food, medical expenses, transportation, and housing, contribute differently to the overall inflation rate.

For retirees, inflation, measured explicitly by CPI-E, can have slightly different implications due to the elevated costs of healthcare and housing. While planning for retirement longevity is crucial, it’s equally important to account for inflation’s impact on your ongoing living expenses.

How Inflation Affects Your Retirement

As time passes, inflation will gradually diminish your purchasing power. This could lead to a widening “income gap” over the years, mainly if you rely on a fixed income. Consider whether your investments will grow sufficiently to offset inflation in your retirement income.

Learn more: Inflation, Stagflation, and Your Retirement.

Retirement Risks

Planning for retirement can be complex. Longer-than-anticipated lifespans, uncertainty about potential changes to Social Security, potential gaps in Medicare coverage, inflation that continues to erode your savings, and an ever-changing economic landscape with issues such as the national debt, cybersecurity risks, pandemics, and geopolitical tensions all pose significant threats to retirees’ financial stability.

While planning for all these variables in advance can be challenging, retirees must take a comprehensive approach when assessing their retirement plans and goals. Considering both current economic conditions and future trends as part of a rational approach allows you to make educated decisions regarding your retirement.

Don’t hesitate to get professional guidance from a fiduciary financial advisor when determining what works best for you and your retirement goals. You can make plenty of intelligent moves now to help secure your financial security later!

Request a no-cost, no-obligation advisor consultation today!

Get StartedSources:

1. https://www.ssa.gov/oact/STATS/table4c6.html

2. https://www.census.gov/data/datasets/2023/demo/popproj/2023-popproj.html

3. Annuity Mortality Table, Society of Actuaries

4. https://www.cbo.gov/publication/62105

5. https://www.investopedia.com/ask/answers/110614/how-social-security-trust-fund-invested.asp

6. Social Security Administration: Social Security History

7. http://ssa.gov/news/press/factsheets/basicfact-alt.pdf

8. http://investopedia.com/articles/personal-finance/022516/will-baby-boomers-bankrupt-social-security.asp

9. Employee Benefits Research Institute. Center for Retirement Research

10. http://healthline.com/health/medicare/does-medicare-cover-long-term-care#eligibility

11. LongTermCare.gov How Much Care Will You Need?

12. Cost of Care Survey: https://investor.genworth.com/news-events/press-releases/detail/1054/carescout-releases-2025-cost-of-care-survey-results

13. https://www.ssa.gov/news/en/press/releases/2026-06-09.html

Subscribe to our newsletter to stay updated.

-

Previous

Most Popular Retirement Articles

-

Next

3 Financial Phases of Life